Dividend Tracker for Canadian Investors

Track your Canadian dividends across RRSP, TFSA, FHSA, and non-registered accounts in one dashboard. Auto-sync Wealthsimple, Questrade, and other Plaid-supported Canadian brokers (search for yours when you connect); add anything Plaid doesn't cover as a manual portfolio. MerryDiv preserves the CAD/USD reporting your broker uses and tags account types so you can filter dividend income by wrapper. Free to get started.

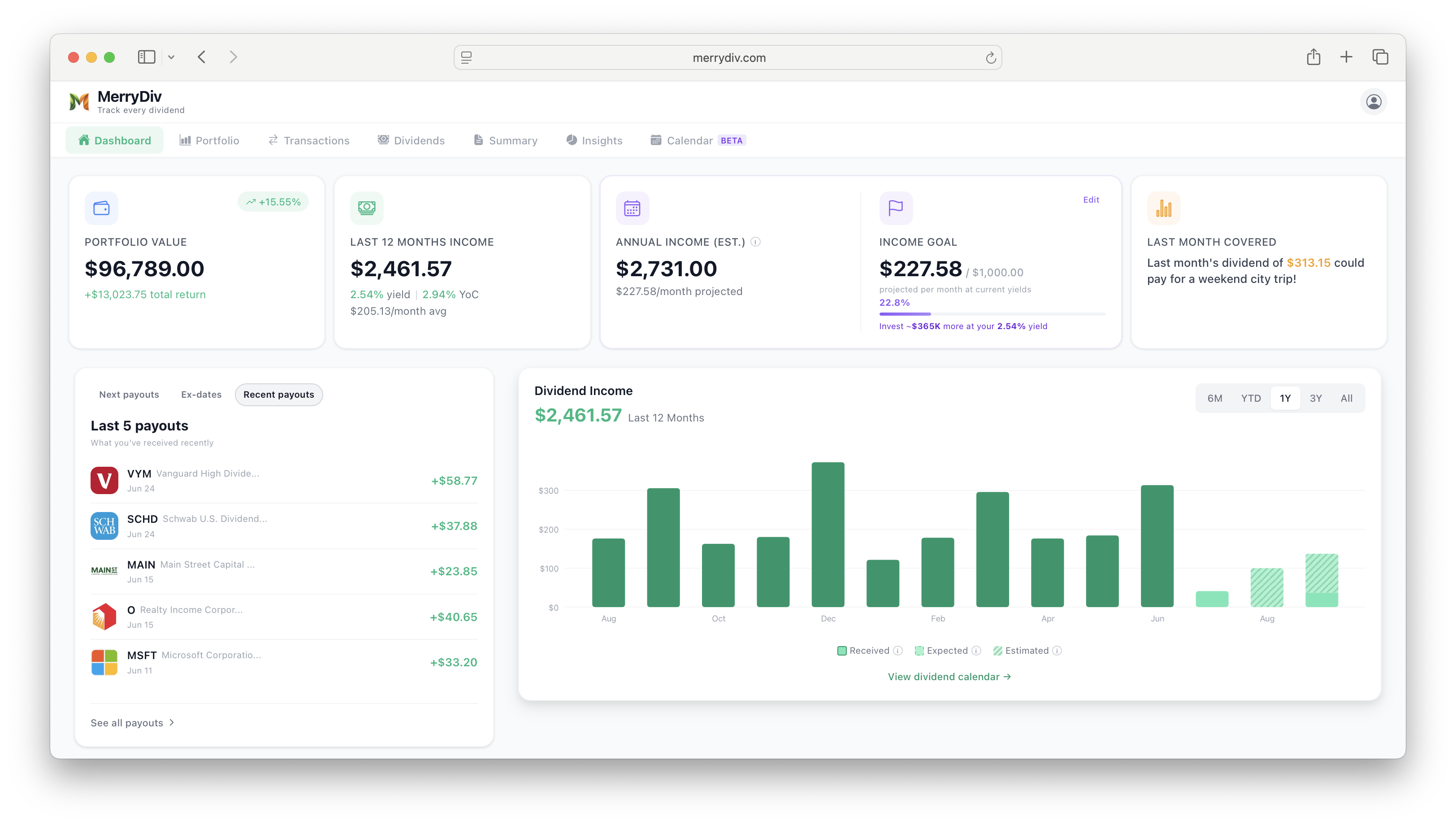

MerryDiv dashboard — RRSP + TFSA + non-registered dividend income in one view.

What MerryDiv syncs

- Dividend payments from Plaid-supported Canadian brokerages, imported automatically — Wealthsimple and Questrade are widely available; search for your specific institution during Plaid Link

- RRSP, TFSA, non-registered (cash / margin), FHSA, and RESP account types

- Both CAD and USD dividend streams — each transaction tracked in the currency Plaid reports from your broker

- Canadian dividend stocks (ENB, BNS, BCE, T, TD, RY) alongside US dividend positions in the same portfolio view

- Canadian dividends alongside US-listed positions in one view — your T5 slip remains the authoritative source for eligible vs. ineligible classification at tax time

Common account types you can track

MerryDiv works with any account your broker exposes through Plaid Link — the picker at connection time shows exactly what's available for your login. Anything Plaid doesn't cover can be added as a manual portfolio.

Canada-specific notes

Canadian dividend tracking has three wrinkles that MerryDiv handles automatically:

- Eligible dividend tax credit. Dividends from Canadian corporations qualify for the enhanced dividend tax credit (gross-up of ~38% and federal credit of ~15% as of 2026 — check the CRA and your province's most recent budget for current rates), while dividends from non-Canadian corporations don't. MerryDiv shows the dividend amount, ticker, and account type in one place; your T5 slip at tax time remains the authoritative source for the eligible-vs-ineligible split.

- US dividends in an RRSP. The Canada–US tax treaty exempts US dividends held in an RRSP from the 15% US withholding tax — but not in a TFSA or non-registered account. MerryDiv tracks the account type so you can see the actual post-withholding amount that landed.

- CAD vs. USD. Many Canadian brokers hold US-listed stocks in both a USD sub-account (avoiding conversion) and a CAD sub-account (with conversion on each dividend). MerryDiv preserves the reported currency for each transaction so your totals match the broker statement, not a converted approximation.

Popular Canadian dividend holdings

Yield, frequency, and annual dividend for each. Click any row for full history and analysis.

Yields shown are snapshot values as of July 2026. Live figures on the stock page for each ticker. Educational examples only — not investment advice or a recommendation to buy any specific security.

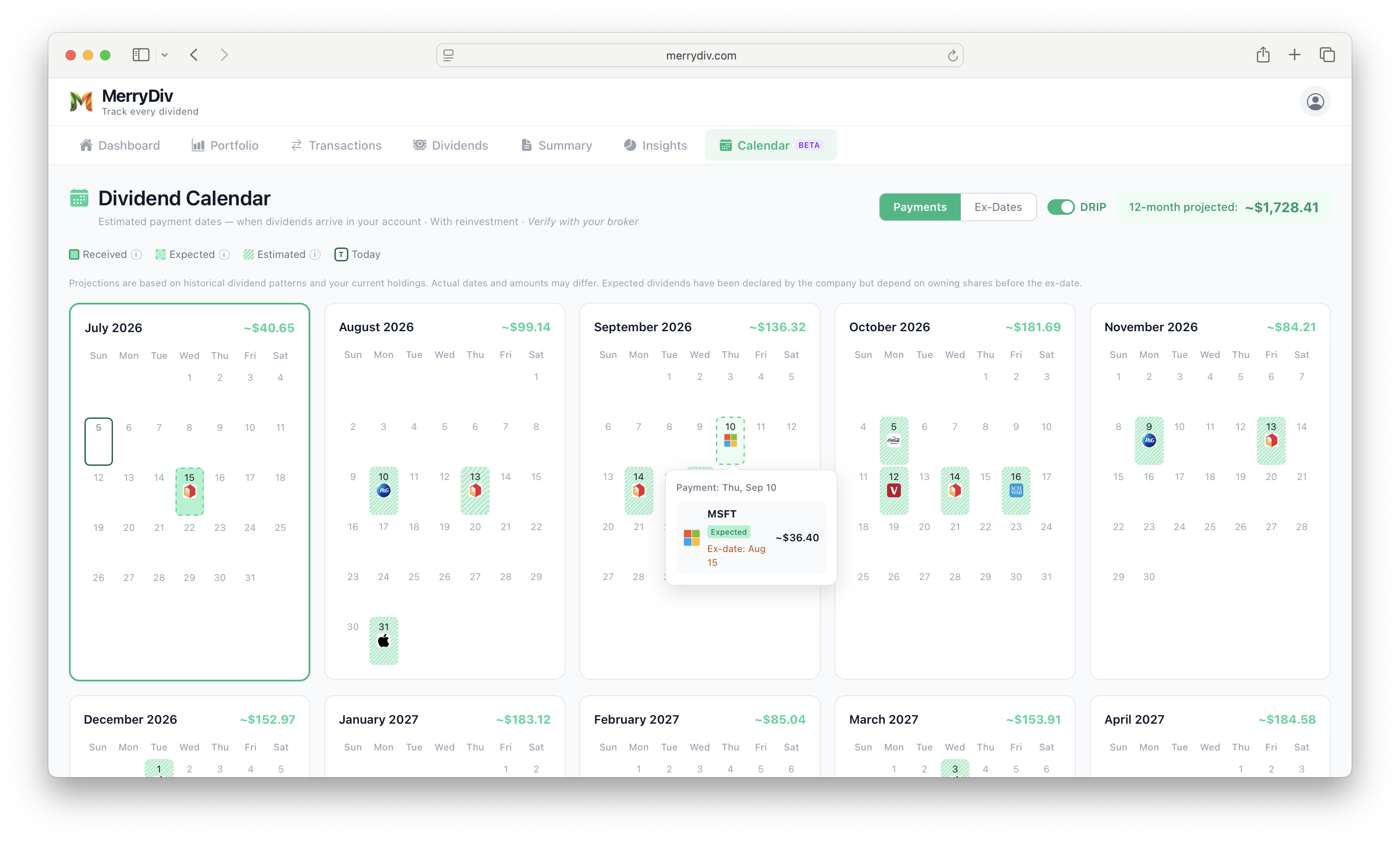

Dividend calendar — every Canadian dividend payment across your accounts, month by month.

How Canadian dividend tracking is different (and why it matters)

Canadian dividend investors have three complications American investors don't: two currencies, three registered account wrappers with different tax rules, and the eligible-dividend tax credit that changes how a Canadian dividend is taxed compared to a foreign one. Native broker dashboards handle each of these poorly, and the mismatch gets worse if you hold accounts at more than one Canadian broker.

The eligible-dividend tax credit — the biggest thing brokers get right (and wrong)

Dividends from Canadian public corporations qualify for the enhanced dividend tax credit: roughly a 38% gross-up and a 15% federal credit (plus provincial credit) as of 2026. For a top-bracket Ontario investor that puts the effective tax rate on eligible Canadian dividends at roughly 39% — compared to roughly 53% on interest income and roughly 46% on U.S. dividends (which don't qualify). Rates change with each federal and provincial budget; consult the CRA and your province's most recent budget for authoritative numbers. The bigger practical issue is that native brokerage dashboards typically don't distinguish eligible from non-eligible dividends in your monthly view — it only shows up on the T5 slip at tax time. MerryDiv doesn't currently split dividends by eligibility classification either; the T5 slip is still the authoritative source at tax time. What MerryDiv does show is the ticker, name, amount, currency, and account type for each dividend, so you can review your holdings and reason about likely eligible-dividend candidates yourself.

US dividends in an RRSP — the 15% withholding tax exemption

The Canada-US tax treaty makes RRSPs special: US dividends held inside an RRSP (individual, spousal, or LIRA) are generally exempt from the 15% US withholding tax that typically applies to the same holding in a TFSA or non-registered account. This is why many dividend-focused Canadians hold their US-listed dividend positions in the RRSP and their Canadian dividend positions in the TFSA. MerryDiv shows the amount your broker reports through Plaid for each dividend transaction, so what you see is what actually landed — as an example, a US-stock dividend of ~$100 USD typically arrives full in an RRSP and around $85 USD after 15% withholding in a TFSA (subject to broker treatment, security type, and any additional FX conversion on the CAD side).

CAD vs. USD dividend accounting

Most Canadian brokers now let you hold US-listed positions in a USD sub-account — avoiding automatic conversion every time a dividend arrives. Questrade, Wealthsimple, TD Direct, and RBC Direct all offer this, though specific account behavior varies. If you're using a broker's default account that converts every US dividend to CAD at whatever rate the broker uses on that day, you're typically losing 1–2% to the spread on every payment. MerryDiv stores each transaction in the currency Plaid reports from your broker, so a USD payment stays in USD and a CAD payment stays in CAD.

Native Canadian broker tools vs. MerryDiv

How the built-in dividend view compares — pooled across the major Canadian brokers.

| Feature | Native broker view | MerryDiv |

|---|---|---|

| Historical dividend list | ✓ | ✓ |

| Eligible vs. ineligible dividend classification | On T5 only | T5 remains authoritative |

| RRSP/TFSA/non-reg wrapper tagging | ✓ | ✓ |

| US withholding tax post-deduction display | Limited | ✓ |

| CAD/USD sub-account currency preservation | ✓ | ✓ |

| Cross-broker rollup (Questrade + Wealthsimple + TD) | ✗ | ✓ |

| Forward income projection | ✗ | ✓ |

| Yield on cost | ✗ | ✓ |

| Upcoming ex-dividend + payment calendar | ✗ | ✓ |

| Export to CSV for T5 reconciliation | ✓ | ✓ |

How to connect your Canadian broker in MerryDiv

- 1Create a free MerryDiv accountEmail + password only — no credit card required.

- 2Click Connect BrokerageThe Plaid picker opens with 12,000+ institutions searchable by name or logo.

- 3Select your Canadian brokerSearch for your institution — Wealthsimple and Questrade are widely available on Plaid Canada; other Canadian brokerages appear as Plaid rolls out Investments coverage. Anything unsupported? Add as a manual portfolio instead.

- 4Choose which accounts to importRRSP, TFSA, FHSA, RESP, non-registered, corporate — pick any combination your broker exposes through Plaid. Anything Plaid doesn't cover can be added as a manual portfolio.

- 5Dividends start syncing automaticallyCAD and USD sub-account amounts preserve the currency Plaid reports from your broker. Your T5 slip remains the authoritative source for the eligible-vs-ineligible dividend classification at tax time.

Canadian dividend stocks Canadian investors often discuss — Big Five banks and beyond

Canada's Big Five banks are the closest thing to a Canadian dividend-aristocrat category: quarterly payments going back decades, rare cuts, and eligible-dividend tax treatment. Five Canadian names frequently discussed in dividend-investing communities — different sectors, different profiles:

| Ticker | Yield | Payout | Category |

|---|---|---|---|

| RY | 3.72% | Quarterly | Royal Bank of Canada — Big Five bank |

| TD | 4.68% | Quarterly | Toronto-Dominion Bank — Big Five bank with US retail-banking footprint |

| ENB | 6.24% | Quarterly | Enbridge — energy-pipeline midstream |

| BCE | 8.42% | Quarterly | Bell Canada — telecom; historically high headline yield with a recent dividend cut in its history |

| BNS | 5.92% | Quarterly | Bank of Nova Scotia — Big Five bank with Latin American exposure |

Yields as of July 2026 and change frequently. This list reflects Canadian names commonly discussed in dividend-investing communities, not MerryDiv user data. Educational examples only — not investment advice or a recommendation to buy any specific security.

RRSP vs. TFSA — where should your dividends live?

Rule of thumb Canadian dividend investors converge on: US-listed dividend positions go in the RRSP (avoids 15% US withholding tax under the treaty), Canadian dividend positions go in the TFSA (tax-free forever, no US withholding to worry about), and non-registered accounts hold whatever's left — with eligible dividends preferred because of the enhanced tax credit. If you're not sure where a specific holding should sit, filter your dividend income by account type in MerryDiv to see the effective yield after tax by account.

Questrade vs. Wealthsimple for dividend tracking

Questrade's ECN commission structure ($0.01/share, capped) is competitive for large-dollar dividend investors who reinvest manually. Wealthsimple's zero-commission Trade is friendlier for smaller lot sizes and fractional-share dividend reinvestment. Both are widely available in Plaid Canada for tracking purposes — specific account-type coverage depends on what your broker exposes through Plaid Link. The real difference between the two isn't the data feed, it's the transaction cost of your reinvestment strategy.

Canadian dividend tax — approximate rates by province (as of 2026)

The federal component of the eligible-dividend gross-up (~38%) and the federal credit (~15%) are the same everywhere in Canada. Provincial credits vary: Ontario roughly 10%, BC roughly 12%, Alberta roughly 9%. Combined, an Ontario top-bracket investor pays roughly 39% on eligible Canadian dividends vs. roughly 53% on ordinary interest income. These rates change with each provincial budget — check the CRA and your province's most recent budget for authoritative numbers before filing.

Frequently asked questions

Track your dividends free

Connect once, see your dividend payments across your connected accounts in one dashboard. Free plan, no credit card required.

Get started for free